Table of contents

- What Is an NFT, and What Does NFT Stand For?

- What Is a Fungible Token?

- A Brief History of NFTs

- NFT Marketplaces

- What Is NFT Minting?

- How Do I Mint an NFT?

- Step 1 - Log in to Your MetaMask Wallet and Connect to Opensea

- Step 2 - Upload Your Digital File in Any Supported Format (Below the max limit of 100 MB).

- How Do I Sell My NFT?

- Can You Make Any Changes to Minted NFTs?

- What Are the Technical Specifications of an NFT?

Non-fungible tokens (NFTs) have taken the world by storm in the past year, appearing at Sotheby auctions and selling for millions.

NFTs have shown the world a new type of ownership that anyone can verify at any time.

The unique properties of NFTs are why we have seen millions of dollars being poured into them.

Owning an NFT can mean many things: collectible items, lottery tickets, access pass, concert tickets.

No one can forge ownership of an NFT. They can only be bought and sold between people. But what are NFTs?

What Is an NFT, and What Does NFT Stand For?

Each NFT is unique. They possess a key property known as the token ID, which is randomly generated and ensures that each NFT is unique.

NFTs take form of digital files - artwork, videography, music.

The digital file is transformed into an NFT and stored on the blockchain, where it lives forever.

No one can remove that NFT now, and because the blockchain is public, you'll be able to see a record of all the previous owners of a certain NFT, and also its current owner.

If someone created a copy of the NFT, we could use its token ID to identify whether or not it's the real NFT. We'll dive into the technicalities of a token ID later in the article.

When distinguishing between real and fake money, we rely on human skills to identify the difference.

The capabilities of verifying whether something is authentic or counterfeit without a human is what makes an NFT much more valuable.

What Is a Fungible Token?

All fungible tokens are the same if they originate from the same smart contract.

A typical example of this is the US dollar.

No matter which dollar you get, it's still worth a dollar. In other words, a dollar still retains the same value, even though the mint number is different.

This is very similar to tokens we see in crypto. Every Bitcoin is identical to another in terms of its value, even if its minting number is different.

This is where it differs with NFTs: NFTs vary in value.

Also, fungible tokens are interchangeable. One Bitcoin can be swapped with another Bitcoin, and we know its value is the same. Whereas NFTs are not interchangeable: each NFT has a different value.

A Brief History of NFTs

NFTs were first-created in 2010, on the Bitcoin network called Colored Coins.

In June 2017, an NFT project called CryptoPunks was the first collection to gain traction and set a standard of 10,000 NFTs.

CryptoPunks might look similar at first glance, but each was unique and completely different from another.

They used Python to program layers of artwork to create each unique piece. However, they didn't follow the ERC-721 convention for NFTs, as it had not been invented yet.

This project had sparked an interest in creating the ERC-721 standard, which now influences digital art and collectibles.

CryptoPunks are now an essential part of NFT history, and their price reflects that. At first, these Punks were free for people to mint, along as you covered the minting cost. Now, these historical NFTs attract outrageous prices.

Following CryptoPunks, CryptoKitties was born in October 2017. CryptoKitties was the first project to follow the new ERC-721 standard, but they weren't just digital images like CryptoPunks.

CryptoKitties is a blockchain game and these NFTs could be used within the game for breeding purposes. CryptoKitties was a pretty simple game, but this new innovation meant that game items (that are NFTs) could now be sold for real money. Previously, on the other hand, gamers would invest money into a game, but the money could be used only within the game, and never taken out.

People were making a lot of money from CryptoKitties, with some selling up to 6 figures, which attracted worldwide news outlets, such as CNBC.

NFT Marketplaces

Following the rise of popularity in NFTs, people started to create more NFT projects.

However, it was not easy to sell these NFTs, which spawned the creation of different NFT marketplaces.

The most popular marketplace to buy and sell NFTs is OpenSea.

OpenSea hosts a majority of NFTs and make it easy to find any collection. OpenSea lets anyone mint an NFT on their website and sell it. Websites, such as OpenSea, make it easy for anyone to mint an NFT onto the blockchain.

There are a variety of NFT marketplaces to mint NFTs, but here are a few with different entry requirements:

OpenSea - Allows anyone to mint NFTs on their website. Rarible - Allows anyone to mint NFTs on their website. MakersPlace - Invite only. Foundation - Invite only. SuperRare - You have to go through an application process.

What Is NFT Minting?

Minting an NFT involves bringing a digital art file, such as an image, gif, or video, and bringing it onto the blockchain.

Once the NFT is brought onto the decentralized network, it will live there forever and can not be removed or modified. Whoever brought the NFT onto the blockchain will have their crypto wallet address tagged to the NFT. This means that even if an NFT is bought and sold between 100+ people, it will still be possible to track it back to the original creator and owner, which displays the originality of an NFT.

It sounds pretty complicated, but fortunately, NFT marketplaces have simplified the process.

Most marketplaces do not charge for minting or listing an NFT. However, there's still a cost to mint your NFT to the network.

Everyone will have to pay a minting cost when they mint an NFT to the network, as you are making a change to the public network by adding your NFT to it.

The cost will depend on the gas price at the time, but can range from 10-100 USD, depending on how busy the network is.

How Do I Mint an NFT?

There are a few different ways to mint an NFT, some involve using code, but marketplaces don't involve code.

Learn how to mint NFTs here.

Whether or not you use code depends on how many NFTs you want to sell. But, for the typical user minting NFTs, it's generally easier to use the marketplaces. This is because the process is simpler, and there aren't any technicalities required.

You may have come across some NFT 10k collections, such as Bored Ape Yacht Club (BAYC) or Cool Cats, which have similar images but differ in accessories.

These collections, similar to CryptoPunks, have been generated using code and then minted by the user on their respective websites.

This is a more complicated way to mint NFTs compared to OpenSea, but this helps the creator avoid paying a lot more in gas fees. Instead, this requires the users buying the NFTs to pay the gas fees, whereas, on OpenSea, the creator pays the fees to list the NFTs. For a 10k collection, that can be very expensive!

Gas fees are how much you pay to interact with the blockchain, and its price depends on how busy the chain is.

Read more about gas fees here.

Let's cover how to mint an NFT using OpenSea, as it's a widely adopted marketplace. There are some pre-requisites to mint an NFT:

- MetaMask wallet or another compatible wallet.

- Ethereum to cover gas fees.

- Digital art file (image, gif, video.

Step 1 - Log in to Your MetaMask Wallet and Connect to Opensea

Then, click "Create" on the top-right corner of the screen, and sign the MM notifications. They'll pop up if it's your first time on the website, as they need to get access to your wallet to perform transactions.

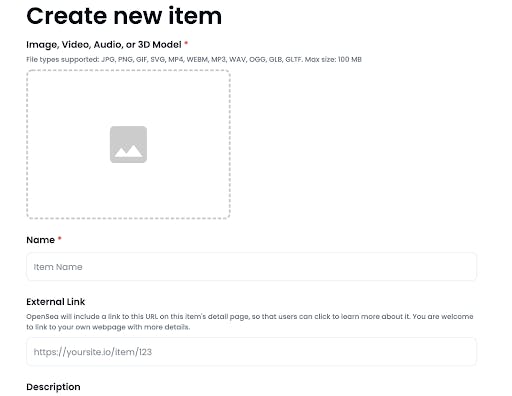

You should now be shown a screen similar to the one seen below:

Step 2 - Upload Your Digital File in Any Supported Format (Below the max limit of 100 MB).

You'll be then required to fill in the rest of the details, such as the name of the NFT, description, and collection name.

You'll notice that other fields, such as properties, levels, and stats are generally used for NFTs in a collection or a game. This helps people see the differences between NFTs, and identify how rare an NFT is due to its properties.

When creating NFTs, keep in mind how many you want to mint, as they can never be destroyed. You can always create more NFTs, but you must decide their rarity. People associate rarity with higher quality or an increased market price, so it's important to know how many of the same NFTs you want to mint.

Next, click "Create". Notifications will pop up on your MetaMask.

If this is your first time creating an NFT on OpenSea, you'll have to sign a transaction in order to authorize your wallet to interact with it, as well as another transaction to mint your NFT into the blockchain.

Once you have accepted these transactions on MetaMask, you should be able to see your NFT in your profile under the "Created" header.

Congratulations!

You have now created an NFT, and it'll forever live on the blockchain.

You can now choose to keep your NFT, or if you want to be a budding NFT artist, try to sell it.

How Do I Sell My NFT?

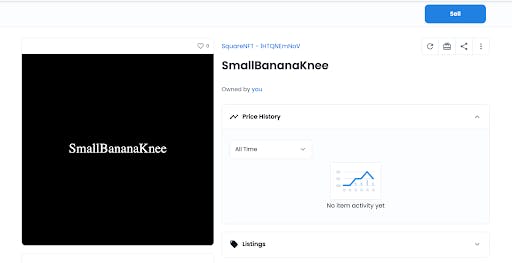

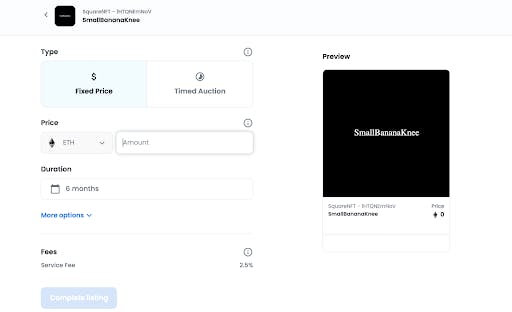

Start by clicking on your newly created NFT; it should open up and display a new page, similar to the one below:

Now click on the "Sell" button, which will bring you to a new page and give you options to sell your NFT. You can either sell your NFT at a fixed price or list it at auction with a starting price and duration.

Most marketplaces on the Ethereum blockchain, like OpenSea, will list prices in Ethereum, so you'll have to choose a price in Ethereum.

Marketplaces on other blockchains such as Tezos or Avalanche will instead have prices in their respective tokens.

OpenSea also takes a 2.5% fee per sale, as you can see below:

There are few fees involved in creating an NFT, so it’s essential to time your interactions with the network when gas fees are low, usually, early in the morning or on the weekend.

Can You Make Any Changes to Minted NFTs?

No.

If your NFT is solely a piece of artwork, it can no longer be modified once it's on the blockchain. However, there are the properties that we looked at before while creating an NFT, such as levels and stats, which be modified if an NFT is used within a game.

The NFT itself won’t change in terms of artwork, but its stats can.

Bored Ape Yacht Club (BAYC) showed another way to make changes to NFTs without actually changing the original, and this was by creating a new NFT collection based on the original collection.

For example, BAYC creators gave each BAYC owner a mutant serum. If used, they would need their original BAYC NFT to create a Mutant Ape Yacht Club, thus spawning a new NFT collection.

The Bored Ape Yacht Club and Mutant Apes Credits: ApeofPoland/Twitter via @ApeofPoland

The Bored Ape Yacht Club and Mutant Apes Credits: ApeofPoland/Twitter via @ApeofPoland

What Are the Technical Specifications of an NFT?

We previously mentioned the ERC-721 standard that NFTs follow, but in this section, we'll dive deeper into the technicalities of an NFT.

The ERC-721 is a set of standards that define an NFT. Once an NFT is put onto the blockchain, this NFT is given a unique property -- a token ID. A token ID is created randomly by combining a bunch of random numbers.

No two NFTs will share the exact value of a token ID.

Each NFT will have a different token ID numbers. That means NFTs can possess a different value even if they come from the same origin.

Let's say you and your friend bought tickets to the same concert. You got ticket #200 and they got ticket #201. The tickets are for the same concert (NFTs), but they have different numbers (token ID).

The token IDs behind these tickets would look completely different, for example:

Ticket #200 - 263747385792398589238990359065706572382398

Ticket #201 - 888964586577348543728840975784395942090239

On the other hand, fungible tokens, such as a Bitcoin or Ethreum possess the same token ID, value, and characteristics. In the case of a fungible token, the token ID looks something like this:

Bitcoin #200 - 1256479329752985928590

Bitcoin #201 -1256479329752985928590

As NFTs possess a unique identifiable value, which means they're able to onboard a lot of physical world items onto the blockchain as a sign of ownership.

When you buy a house or car, paperwork is transferred over to you, but if that paperwork gets lost or systems go down, there is no proof of ownership.

There are cases where, due to lost paperwork decades or centuries ago, there are pieces of land no longer owned by anyone, as there is no longer proof of the ownership of the land.

If ownership of a house, for example, was on the blockchain, you could always prove that it's your house. When you decide to sell it, you'll just need to transfer the digital file over to the new owner to show proof that they're the new owner.

It will be a long time before something like this is implemented, but it shows the power of NFTs and how they could be used in the future.

This article is a part of the Hashnode Web3 blog, where a team of curated writers are bringing out new resources to help you discover the universe of web3. Check us out for more on NFTs, DAOs, blockchains, and the decentralized future.